.avif)

%20IMAGE%20(1).png)

.webp)

Fully compliant. Funds settle into your Client Account without delay, strictly adhering to MEAS Standard 9.

Funds are never commingled. They are processed securely by CHIP and reconciled into your account by the next business day.

Zero transaction fees. Buyers pay the exact deposit amount, and agencies pay nothing to receive it.

We partner with Bank Negara registered payment gateway (CHIP IN Sdn Bhd) to ensure competitive rates, rapid settlement times, and direct local support.

Agencies are reporting institutions. We automate your specific compliance obligations under the AMLA 2001 Act.

Streamlined process. You only need to upload the OTP/OTR to link the deposit; no duplicate document uploads required.

Your commissions are untouched. We monetise downstream valuation leads via ValuationXchange and bank partners.

You stay in control. We identify risks, but your agency decides whether to proceed or refund based on your internal SOPs.

Audit-ready clarity. Bank statements clearly show "CHIP" transfers, supported by downloadable reconciliation reports.

FPX is standard. Credit card payment options for international clients are scheduled for release in Q1 2026.

Be part of the movement for transparent,

tech-enabled valuation in Malaysia.

Johor’s property cycle is gaining pace, but the credit risks begin upstream of underwriting. In the October 2025 PEPS Ventures webinar supported by ValuationXchange, Dr. Lee Nai Jia (PropertyGuru Group) and Sr. Samuel Tan (Olive Tree Property Consultants) highlighted how marketing rebates embedded in Sale & Purchase Agreement (SPA) prices, misused “indicative values,” and offline, non-traceable workflows can distort collateral quality for banks in Malaysia.

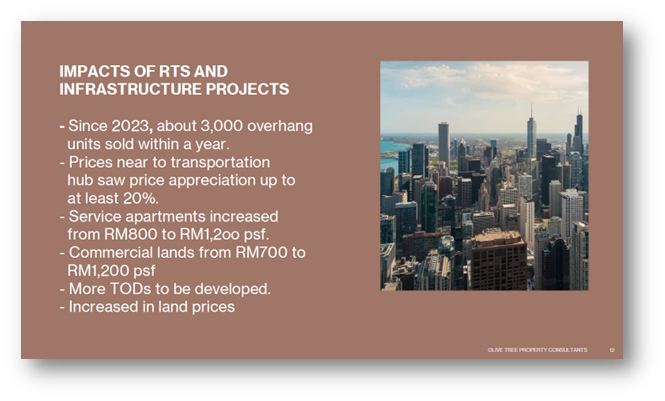

Market context matters for risk models: demand around major infrastructure (RTS/JS-SEZ) has pushed certain sub-markets higher, e.g., serviced apartments moving from ~RM800 to ~RM1,200 psf and commercial land from ~RM700 to ~RM1,200 psf; while Johor’s residential overhang has fallen (≈3,030units), signalling faster price transmission. Without disciplined, net-of-rebate evidence and transparent processes, inflated benchmarks can migrate into comparables and loan-to-value (LTV) decisions.

This article is part of our Johor webinar series. For cross-border demand dynamics, see Series 1 - “Singapore’s Influence on Johor Property: What Banks and Valuers Must Watch.”

Ready to Elevate Trust in Property Valuation?Join the #TransformationTribe and discover how ValuationXchange empowers smarter lending through trusted, tamper-proof, and transparent valuation workflows.

Reach out to our team to explore how we can support your valuation, compliance, or risk management transformation.

.avif)

.png)