.avif)

.webp)

Fully compliant. Funds settle into your Client Account without delay, strictly adhering to MEAS Standard 9.

Funds are never commingled. They are processed securely by CHIP and reconciled into your account by the next business day.

Zero transaction fees. Buyers pay the exact deposit amount, and agencies pay nothing to receive it.

We partner with Bank Negara registered payment gateway (CHIP IN Sdn Bhd) to ensure competitive rates, rapid settlement times, and direct local support.

Agencies are reporting institutions. We automate your specific compliance obligations under the AMLA 2001 Act.

Streamlined process. You only need to upload the OTP/OTR to link the deposit; no duplicate document uploads required.

Your commissions are untouched. We monetise downstream valuation leads via ValuationXchange and bank partners.

You stay in control. We identify risks, but your agency decides whether to proceed or refund based on your internal SOPs.

Audit-ready clarity. Bank statements clearly show "CHIP" transfers, supported by downloadable reconciliation reports.

FPX is standard. Credit card payment options for international clients are scheduled for release in Q1 2026.

Be part of the movement for transparent,

tech-enabled valuation in Malaysia.

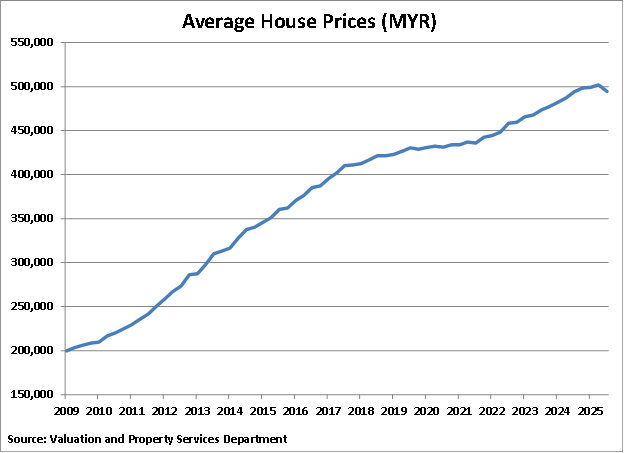

In recent years, gold prices have climbed steadily, often interpreted as a response to inflation, currency movements, and broader economic uncertainty. At the same time, residential property prices in Malaysia have also continued to trend upward, drawing attention from buyers, investors, and industry participants alike.

While gold and property operate in very different markets, their recent price movements offer an interesting comparison. Not because the two assets are directly linked, but because both reflect how markets respond when purchasing power changes over time.

Gold is widely viewed as a reference point for value preservation. When inflation expectations rise or confidence in currency weakens, gold prices tend to adjust quickly. There is no financing structure involved, no ability to smooth out price movements over time. The adjustment is immediate and visible.

As a result, rising gold prices are often understood as a signal - one that reflects changing perceptions around money, inflation, and long-term value rather than short-term speculation.

Property markets, by contrast, respond to similar pressures in a different way.

Rather than adjusting purely through price movements, property prices are shaped by a combination of demand, supply, and financing structures. Over time, longer loan tenures, higher loan amounts, and various financing arrangements have helped support affordability at a monthly level, even as headline prices rise.

These mechanisms are not unique to Malaysia, nor are they inherently negative. They play an important role in maintaining market participation and supporting homeownership. At the same time, they mean that property prices do not always move in lockstep with income growth or changes in purchasing power.

In this sense, property prices increasingly reflect how financing capacity evolves alongside market conditions.

This helps explain why gold prices and property prices can rise during the same period.

Gold tends to respond directly to shifts in monetary conditions.

Property adapts to those shifts through financing structures that spread costs over longer horizons.

Both assets are responding to similar underlying pressures, but through different mechanisms. Gold reflects these pressures through immediate price changes, while property reflects them through gradual adjustments in loan structures and transaction dynamics.

The result is that prices in both markets can move higher at the same time, even though the forces driving them are not identical.

For buyers and investors, the key takeaway is not that rising property prices are inherently problematic, but that price movements should be interpreted in context.

Headline prices alone do not always capture the full picture. Financing terms, valuation methods, and transaction structures all influence how prices are formed and how risk is distributed over time. Understanding these elements can help buyers and investors make more informed decisions, particularly in markets where prices have risen significantly over longer periods.

As property markets become more complex, clarity around valuation and transaction processes becomes increasingly important. Clear documentation, transparent valuation workflows, and consistent information help all parties better understand how value is assessed and communicated.

In this context, platforms like ValuationXchange focus on supporting clearer, more structured property transactions by improving visibility and trust across the valuation process. This allows buyers, sellers, and professionals to engage with the market with greater confidence and understanding.

To learn more about how ValuationXchange helps bring clarity that builds trust across property transactions, visit valuationxchange.com/about-us.

Ready to Elevate Trust in Property Valuation?Join the #TransformationTribe and discover how ValuationXchange empowers smarter lending through trusted, tamper-proof, and transparent valuation workflows.

Reach out to our team to explore how we can support your valuation, compliance, or risk management transformation.

.avif)

.png)